The Economic Cause of War: An Hypothesis

ONE of the most obvious facts about international wars, at least those of modern times that must be financed, is that they occur in cycles. From this category must be excluded mere tribal conflicts, and also such military operations as those of Great Britain in the Sudan and in Zululand, and of the United States among Western Indians.

During the last two hundred years, to go no furt her back, three such cycles

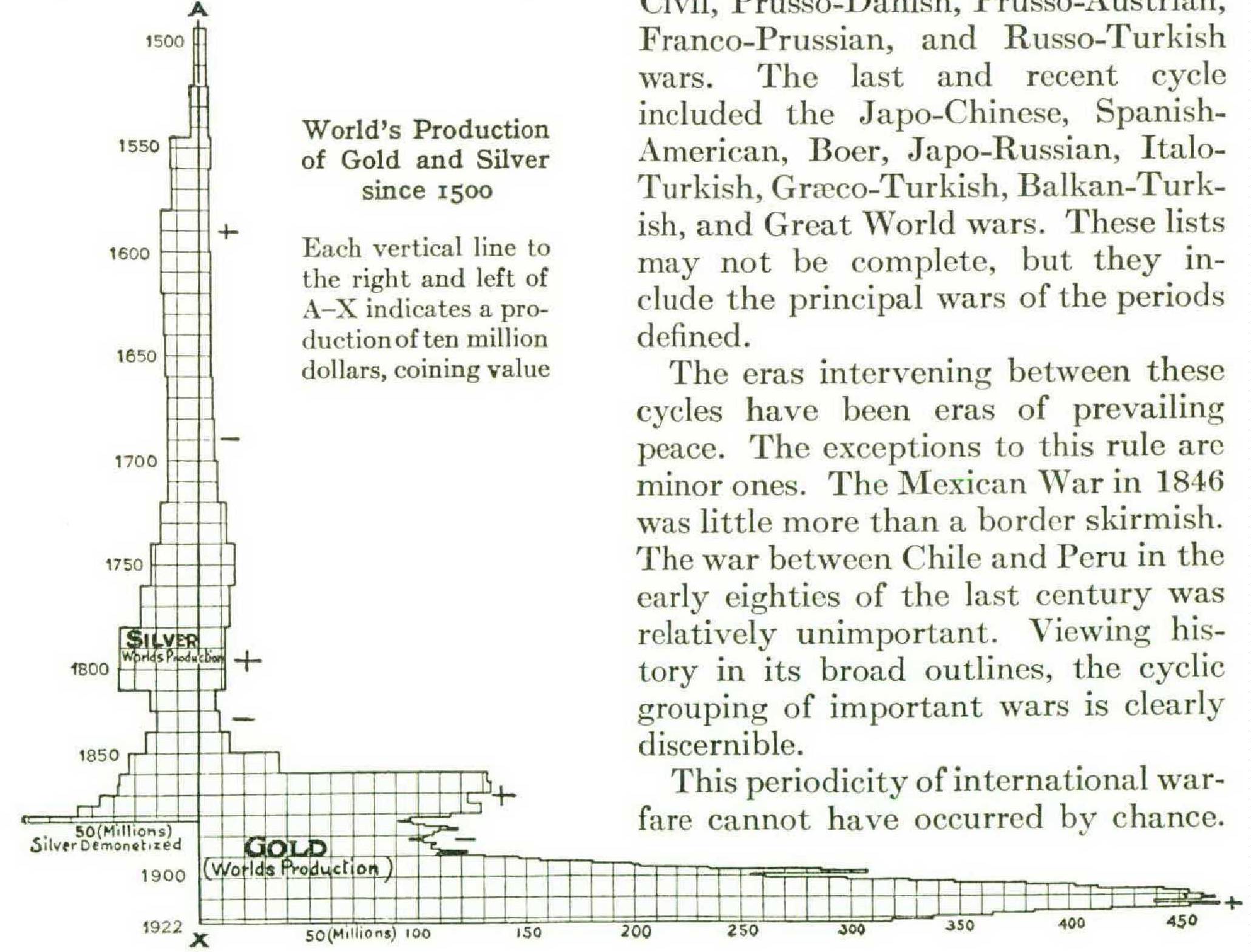

World’s Production of Gold and Silver since 1500

Each vertical line to the right and left of A—X indicates a production often million dollars, coining value

have occurred, the first between 1701 and 1814, the second between 1854 and 1877, and the third between 1894 and 1918.

The first cycle included the War of the Spanish Succession, the First Seven Years’ War, the Second Seven Years’ War, the American Revolution, the French Revolution, and the Napoleonic Wars. The second cycle included the Crimean, Franco-Austrian, American Civil, Prusso-Danish, Prusso-Austrian, Franco-Prussian, and Russo-Turkish wars. The last and recent cycle included the Japo-Chinese, SpanishAmerican, Boer, Japo-Russian, ItaloTurkish, Græco-Turkish, Balkan-Turkish, and Great World wars. These lists may not be complete, but they include the principal wars of the periods defined.

The eras intervening between these cycles have been eras of prevailing peace. The exceptions lo this rule are minor ones. The Mexican War in 1840 was little more than a border skirmish. The war between Chile and Peru in the early eighties of the last century was relatively unimportant. Viewing history in its broad outlines, the cyclic grouping of important wars is clearly discernible.

This periodicity of international warfare cannot have occurred by chance.

It indicates an economic cause that works in cycles.

In the physical sciences, the periodicity of phenomena is regarded as a fact of great significance. When yellow fever was the great scourge of tropical countries, it was known to be a seasonal disease. It spread with the coming of summer and abated with the first frosts of autumn. It was this periodicity, perhaps more than any other clue, that led to the detection of the Stegomyia mosquito as the disease-carrier. In other words, in looking for the cause of the periodicity of the disease, the cause of the disease was discovered.

So if we are successful in ascertaining the cause of the periodicity of warfare we may expect to identify also the economic cause of war. We must look not only for a cause operating in cycles, but also for one that operates in irregular cycles. In other words, the cause, when found, must explain the irregularity and speeding-up of these cycles during recent decades. In addition we must look for a world-wide cause, since the tendency to warfare, when the war cycle recurs, is too general to be traced to any one nation or locality.

I

In searching for a cause of war that answers to these various tests, there are certain causes popularly assigned that must be excluded. Human depravity must be excluded, for human depravity, such as it is, shows no world-wide periodicity in its manifestations. It is a constant quantity. For the same reason the ambition of rulers must be excluded. If the ambition of Napoleon tends to explain the Napoleonic Wars, it cannot account for the American Revolution, the French Revolution, and the other wars of that cycle. For a similar reason we must exclude military and naval armaments, since they reveal no such cyclic arrangement. Military preparations are fairly constant. Armaments are always somewhere being strengthened.

It would be accurate to say that the periodicity of warfare is due to the periodicity of the war complex, meaning thereby the resultant of those psychological tendencies that are conducive to war. Every era has its own psychological trend. The Germans call it the Zeitgeist. The English call it the spirit of the times. Everyone whose memory goes back thirty years or more knows that the war which was possible in 1914 would have been quite impossible in 1894, or even in 1924. The mood of the world in 1914 was entirely different from what it was at either other date.

But having traced the war cycle to the age psychology, the solution itself needs solving. What underlying cause or condition produces the varying world-mood that makes war possible if not probable in one era and improbable if not impossible in another?

I am not aware that economists have answered this question or even recognized the facts upon which it is based. So I am unable to cite authorities in support of the hypothesis herein suggested. My hypothesis is based upon what was to me a chance discovery made in the course of investigating another subject. This discovery was that for at least two hundred years last past the war cycles have practically coincided with the eras of rising prices, and the eras of rising prices have in like manner coincided with the peaks in the production of the money metals — gold and silver during days of bimetallism, and gold alone since then.

I present herewith a chart of the world’s production of gold from the discovery of America to and including the year 1922, which shows the peaks and the valleys in the production of the precious metals during the period covered. The world’s production of silver is shown only from 1492 till its demonetization by the United States in 1873. At that time it ceased to be basic money and, while it is still used as a money material, its current value is measured by gold.

The production of gold is shown on the right of the line A-X and that of silver on the left. Each vertical line to the right and left of A-X indicates a production of ten million dollars, coining value. Each decade from the year 1500 down is indicated by a horizontal line.

There have been four well-defined peaks of production which I have marked on the margin by the sign for plus. The first occurred during the sixteenth and the first half of the seventeenth centuries. It was due partly to loot from the New World, but principally to the discovery of the silver mines of Potosi and the almost coincident discovery of the method of recovering silver from its ores by the use of quicksilver. The second peak occurred during the eighteenth and the first decade of the nineteenth centuries, ft was due to the progressive development of mines in Spanish America, and fell off rapidly when Spain lost her American colonies in the early part of the last century. The third peak followed the placer discoveries in California and Australia near the middle of the nineteenth century. The fourth peak reached its pinnacle in the year 1915. It has been due principally to the gold discoveries in South Africa and Alaska and the cyanide process of reducing gold from its ores. The valleys of production are marked in the margin by minus signs.

With this chart anyone can make the same discovery that I did. If he investigates the historical facts of the period covered thereby, he will find that the eras of rising prices have coincided, barring possibly a slight lag, with the ascending peaks of money-metal production, and that falling prices in the same manner have coincided with their descent. He will also discover that the war cycles have coincided quite closely with these peaks.

The business of owning and operating gold and silver mines used to be a governmental function. They were reserved from all grants of land. When the gold-miners of 1849 exploited the placer deposits of California, they were technically trespassers on the government domain. But there had been such a gold famine for many years preceding that the United States was only too anxious to have the exploitation continue. In 1806, however, the United States abandoned its former policy of reservation and passed its first law permitting the location and purchase of its gold and silver mines. In most of the British Colonies the same freedom of exploitation and purchase has been permitted.

This change from governmental to private operation has resulted in the quicker exhaustion of newly discovered mines. It is the policy of mining companies to work out a deposit as quickly as possible, thus saving on the ‘overhead.’ The cream of the placers of California and Australia was taken out in twenty years. The Klondike was exhausted in less time. Nome has been decadent for many years. South Africa is reported to have passed the peak of its production.

This speeding-up of the work of goldmining during the last seventy-five years has resulted in greater and more frequent peaks of production and intervening valleys of shorter length, but the peaks still coincide with the eras of high prices and of wars, and the valleys with the eras of falling markets and of peace.

II

It is fair then to conclude that in the recurring peaks of money-metal production we have found the cause of the recurring war-cycles and hence the economic cause of war itself. The chart shows that this cause has operated in irregular cycles and more frequently during the last seventy-five years. Moreover, it is a world-wide cause, for nothing else affects so many people in so many places as a change in the value of the world’s basic money.

Gold measures the prices of commerce, the market value of all accumulated wealth, the monetary consideration of every contract, and the value of all kinds of credit money, whether made of paper, silver, copper, or nickel. Even in the case of depreciated paper-money, it is gold that measures the extent of the depreciation. Let a new and important source of gold be found, such as was the Rand thirty years ago, and presently the whole commercial world will feel the change. The price index will slowly climb, and the rising market will bring hoarded money into active circulation.

If it were possible, by human agency, to alter the force of gravity, so that the pound, ton, or kilogramme would mean one thing one year and an entirely different thing the next, the whole world would combine to prevent by law any such interference. But, while standards of weight are beyond the reach of human tampering, the standard of value is not. Nothing is more certain than that an overproduction of gold will cheapen the world’s money and will bring an era of rising prices in every nation using gold as money.

The reasons assigned for the rise of prices—the ‘high cost of living’ in popular phrase — during the twentieth century are legion. There is scarcely a man afflicted with such poverty of thought as not to possess a fluent explanation of the cause of high prices. But here is one fact that is worthy the attention of every thinking man: the entire world’s production of gold from the discovery of America to the close of the year 1923 was, in round numbers and in American money, nineteen billion dollars; of this aggregate amount, more than one half has been produced since the year 1896. Such a stupendous production of the money metal in so short a time is without precedent in all human history.

If it pleases a man to have his pet theory as to the rise of prices during the twentieth century, I should not refuse him. If it pleases many men to have many differing theories, they are within their rights. But Professor Jevons more than fifty years ago dealt with that kind of folk: —

I have only to ask those who think that the growth of population, the increase of demand, or the progress of trade is the cause of the rise in prices, whether population, demand, trade, and so forth, were not expanding before 1849, not so rapidly as since, but still expanding; and how it is that causes of the same kind have produced falling prices before 1849 and rising prices since? ... It may be safely said that the odds are ten thousand to one in favor of a real depreciation of gold. The meaning of this is that the chances are ten thousand to one against a series of disconnected and casual circumstances having caused the rise of price, — one in the case of one commodity, another in the case of another, — instead of some general cause acting over them all.

If a cheapening of the world’s money produces those psychological reactions that generate war, then the wise thing for the world’s statesmen to do is to stabilize the world’s money. We have laws to protect against counterfeiters and similar gentry who would debase our money, but the nations have given the gold-miner carte blanche to cheapen our basic money by overproduction if he can, and the world’s experience since 1896 shows that he can. Some attention should also be given to the men who waste gold in the unnecessary gilding of things.

For fourteen years before the war, Great Britain had permitted the most reckless overproduction of gold in South Africa. The resulting rising markets of that era enormously stimulated British commerce. But they stimulated the commerce of other nations as well, and brought about that commercial rivalry, that intoxication of prosperity, and that desire to grab territory, which were the root causes of the war. As a result of its lack of vision, Great Britain came out of the war with an enormous debt, with its financial primacy threatened if not lost, with its commerce greatly impaired, and with the gold of South Africa in the vaults of the United States. If this gold had been kept in the storehouses of nature and paid out into the channels of trade as it was really needed, it might have given the world the glow of an even and normal prosperity for a century to come. Instead, it was dumped as it was produced, in disregard of its economic effects, and the commercial frenzy thereby produced was followed by the frenzy of war.

The place to stabilize money is at the gold mine and in the factories where gold is wasted. I have no sympathy with those economists who claim that the government must permit everyone to use gold freely in any and every way he may please in order to preserve its value as money. If it should be found that the restriction of the unnecessary uses of gold in the arts cheapens it, that would be a desirable thing to know, since such an effect could be easily remedied by curtailing the production at the mine, a very wise thing to do if we are to consider the future welfare of the race.

For more than thirty years the writer has been a mining lawyer in the largest mining district of the United States, if not of the world. My clients have been largely gold-miners. It has been my business to show them how mining deposits can be located and titles acquired from the government. I am sure that no one would profit more from the stabilization of the value of gold than the gold-miner himself. And it seems to me a most feasible thing to accomplish, but I can see how it will require international cooperation, at least between Great Britain and the United States, the two principal gold-producing countries.

III

We use a thermometer to let us know the condition of things in the distant furnace. The price index is the thermometer of gold-production. Between 1873 and 1894 the price index was warning us that the production of gold was scant. After a few years of approximate stability, it began to warn us that gold was being produced in excessive amounts. The nations of the world gave no heed whatever to these warnings. They seemed and still seem to regard the price index as a matter of only academic importance.

The cyclical fluctuations in prices herein referred to should be distinguished from the seasonal price-fluctuations that largely counteract each other. There is the same distinction between them that there is between ocean waves and ocean tides. Both are waves in the last analysis, but the former are local, and their force is quickly spent, while the latter are broad movements of the whole ocean’s surface, lasting for hours.

Seasonal fluctuations in prices are hound to occur under the most stable money. They are not detrimental but rather beneficial in their economic effects. They give life to trade and bestow their rewards on the keenest trader.

But it is otherwise with cyclical price-movements. They last for years, abnormally stimulating trade and industry on their rise and abnormally depressing them on their fall. They are essentially evil in their effects, and tend to breed social discontent. In so far as they are due to fluctuations in the world’s supply of gold, there ought to be some cure for the evil, and I am optimistic enough to believe that a cure will be found when the ailment is correctly diagnosed. Both diagnosis and cure, however, are rendered the more difficult by conflicting class-interests. Men see quickly what it is to their interest to see. Farmers generally, being producers and property-owners, rejoice in rising prices, while wageand salaryearners complain. If the latter can maintain the wage scale and continuity of employment, they view falling markets with great satisfaction. Hence the two classes see opposite sides of the economic shield, and agricultural sections work more or less at cross purposes with industrial centres. Stable money, based on a stabilized gold supply, would minimize this conflict and do more than anything else could do to bring lasting contentment to both classes.

The tidal-wave price-fluctuations of the twentieth century have caused and are still causing many economic effects other than war, which I cannot point out here. My present purpose is to show that high prices are not so much caused by war as war is caused by high prices, and that in causal effect an era of increased basic-money production precedes both.

Among the many wars of the last four centuries, three stand preeminent as wars of excessive destruction and exhaustion — the Thirty Years’ War, the Napoleonic Wars (considered as a single martial era), and the Great World War. Each of these, like an army of furies from Hell, bestrode the summit of a great money-metal production. And as the last of these terrible conflicts recedes in the near background of memory it becomes mankind to inquire why the very culmination of the most stupendous gold-production of all time should find the leading nations of the world springing at each other’s throats in the most deadly and destructive conflict of all human history.

When once that inquiry is rightly answered, we shall then know the economic cause of war.